Average True Range Indicator Thinkorswim

Average True Range Using The Atr Indicator In Your T Ticker Tape

Average True Range Atr Breakouts Indicator For Thinkorswim Usethinkscript

Average Daily Range Indicator For Thinkorswim Usethinkscript

Calculating 20 Day Atr Futures Io

Atr Based Support Resistance For Thinkorswim Usethinkscript

Average True Range Atr Implied Move For Thinkorswim Usethinkscript

The average true range study has been merged with atr wilder to form the new atr indicator.

Average true range indicator thinkorswim. Please hit the like share and subscribe. How to use the average true range indicator atr duration. In this situation current trend might be. Based upon the classic average true range study which is believed to be a measure of volatility the mtr introduces a new approach to using it.

The difference between the current high and the current low. It is typically derived from the 14 day moving average of a series of true range indicators. True range is the greatest of the following. Supporting documentation for any claims comparison statistics or other technical data will be supplied upon request.

In the new version of the study you can specify which type of the moving average you prefer to use in the calculation. Thank you for watching. The range indicator is a trend following study based on observation of changes in true range and interday range difference between close prices of two adjacent bars. The average true range atr study calculates the average true price range over a time period.

When intraday ranges are considerably higher than the interday ranges the market is said to be out of balance and the range indicator values are high. Just a side note if this helps any. Td thinkorswim tutorial 2020 thinkorswim day trading set up scanners indicators on demand etc. The difference between the current high and the previous close.

Average true range atr is a technical indicator measuring market volatility. The difference between the previous close and the current low. The indicator shown in the chart shows the average daily range for cl was 1 52 points over the last 20 days and 1 52 points over the last 10 days.

Short Term Market Volatility Indicator For Thinkorswim Usethinkscript

Atr Average True Range Thinkorswim Tutorial Youtube

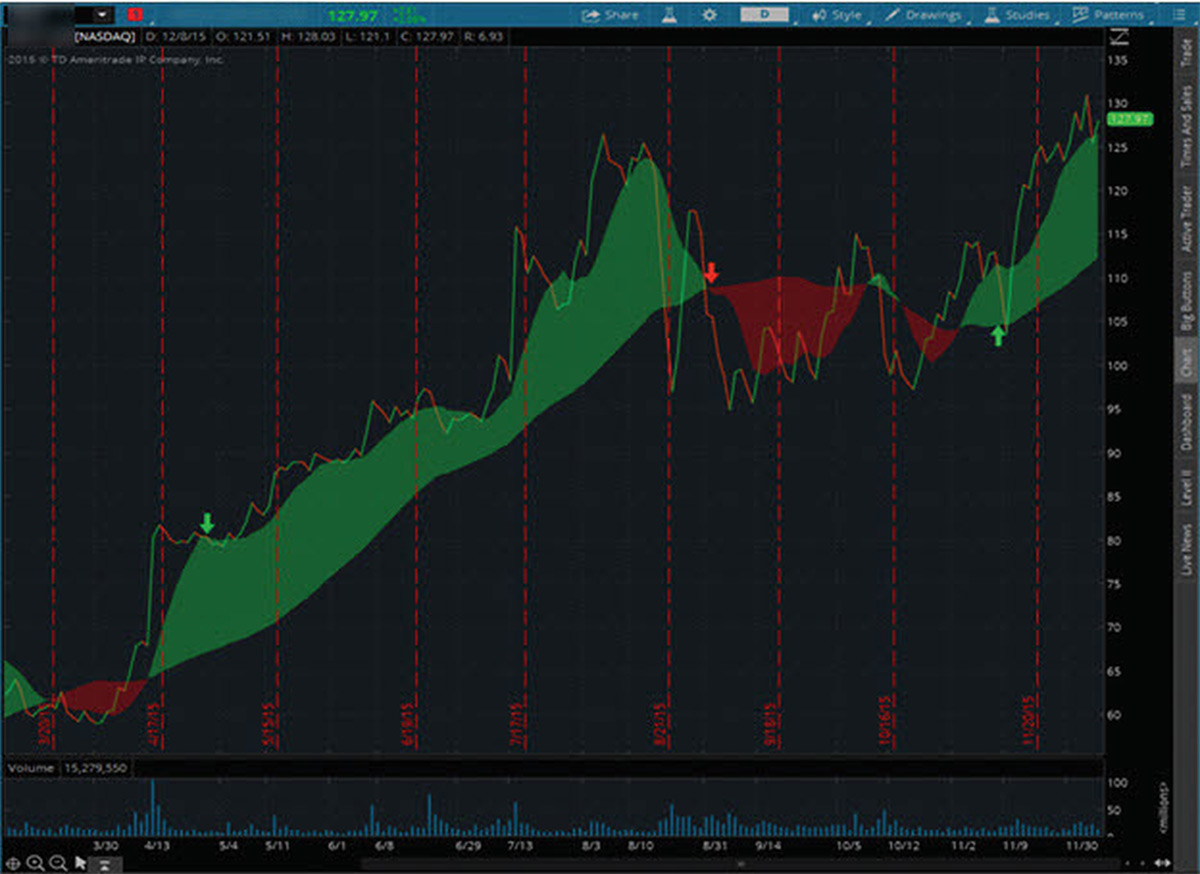

Traders Tips November 2015

True Momentum Oscillator For Thinkorswim Usethinkscript

Tos Thinkorswim If And Ricardo Santos Tradingview

Custom Thinkscript Volume Stats For Thinkorswim Youtube

Multi Time Frame Mtf Braintrend Indicator Thinkorswim No Repaint Version

Averange True Range Indicator O Atr Thinkorswim Tutorial En Espanol Stocks Option Charts Youtube

3 Top Indicators To Use On Thinkorswim Youtube

What Is A Good Relative Strength Index Number Crossover Alerts On Thinkorswim Radio Hemicycle

Charts That Rule The World A Thinkorswim Special Focus Ticker Tape

Multi Time Frame Mtf Atr Indicator For Thinkorswim Tos

How To Choose Technical Indicators For Analyzing The Ticker Tape

Thinkorswim Bid Ask Spread Lines Indicator Column

Getting False Charting Signals Try Out Indicators Of Ticker Tape

Traders Tips August 2013

Relative Volume Indicator For Thinkorswim Easycators Thinkorswim Downloads

My 6 Indicators For Tos For Every Day Thinkorswim By Thetrader Aug 2020 Medium

/DetrendedPriceOscillator-2e28aa89d7f248818cde5ed4bdf9e758.png)

T3 Indicator Thinkorswim The Absolute Best Indicators For Trading Anchorage Sheds

Three Indicators To Check Before The Trade Ticker Tape

Trend Magic Indicator For Thinkorswim Tos

Atr Volatility Based System Indicator For Thinkorswim Usethinkscript

Sierra Chart Daily Atr Levels Indicator Youtube

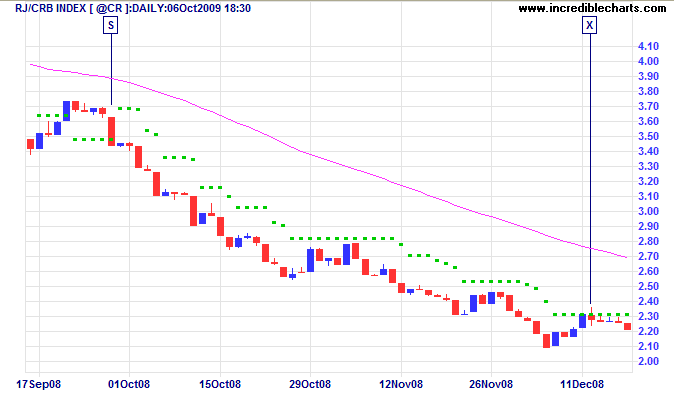

Incredible Charts Average True Range Atr Trailing Stops

Volume Spread Analysis Vsa Reversal Indicator For Thinkorswim Usethinkscript

5dma Scalping Strategy With Indicators For Thinkorswim Thinkorswim

Best Scan For Thinkorswim Forex Trading Signal Group Olphil S Cafe

Ttm Squeeze Thinkorswim Default Indicator By Ogik Tradingview India

:max_bytes(150000):strip_icc()/dotdash_Final_Advantages_of_Data-Based_Intraday_Charts_Jun_2020-03-be9c241d551a48f08104461a4b5282fa.jpg)

Thinkorswim Aggregation Period Wtd Renko Chart Mobile

Currentdayohl With Average Daily Range Futures Io

Thinkorswim Chart Show Current Price How To Use Renko And Heiken Ashi Radio Hemicycle

Thinkscript Read The Prospectus Page 4

Stocks Commodities Magazine

Trend Trader Indicator Suite Free For Thinkorswim Thinkorswim

Thinkorswim Scanner Minimum Atr Value For The Specified Time Period

Think Or Swim High Accuracy Day Trading Strategies Hawkeye System Hormitec Cl

How To Use The Heat Map On The Thinkorswim Platform

Futures 4 Fun Trading Futures With Monkey Bars Ticker Tape

Atr With Standard Deviation And Average For Thinkorswim Usethinkscript

How To Add Chart Labels In Thinkorswim Iv Chart Label And Atr Chart Label Youtube

Position Sizing Calculator For Thinkorswim Usethinkscript

Average True Range Using The Atr Indicator In Your T Ticker Tape

Using Average True Range