Average True Range Percentage

:max_bytes(150000):strip_icc()/ATR-5c535f8fc9e77c000102b6b1.png)

Average True Range Atr Definition

What Is Average True Range Fidelity

Average True Range Atr Chartschool

How To Use Average True Range True Trading Strategies Average

Moving Average Strategies For Forex Trading

True Strength Index Tsi Technical Indicators Indicators And Signals Tradingview

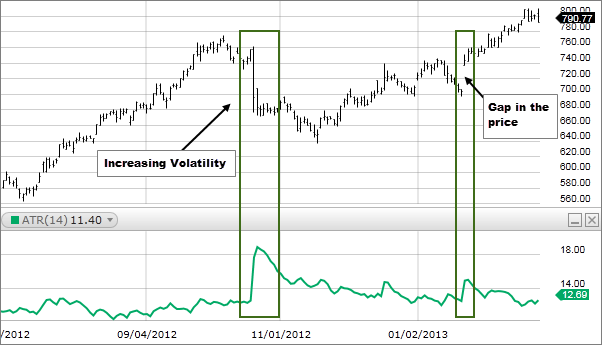

Atr measures volatility taking into account any gaps in the price movement.

Average true range percentage. Description average true range percent atrp expresses the average true range atr indicator as a percentage of a bar s closing price. It is typically derived from the 14 day moving average of a series of true range indicators. Typically the atr calculation is based on 14 periods which can be intraday daily weekly or monthly. The 14 day atr is the average of the daily true range values for the last 14 days.

Average true range atr is a technical indicator measuring market volatility. How this indicator works. The average true range formula looks as. Moving average envelope mae moving average envelopes are lines plotted at a certain percentage above and below a moving average of price.

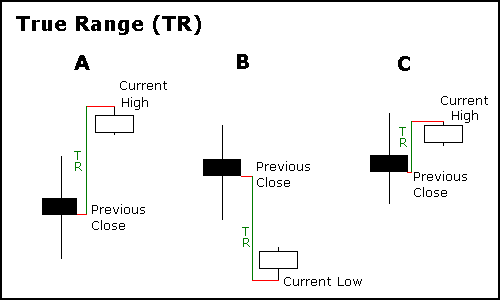

To form the beginning the first true range value is calculated as the high minus the low. The average true range percent is the classical atr indicator normalized to be bounded to oscillate between 0 and 100 percent of recent price variation. Atrp allows securities to be compared where atr does not. As is it average true range of an instrument can be easily compared to any other because of absolute percentage variation and not prices itselves.

Atrp is used to measure volatility just as the average true range atr indicator is. To measure recent volatility use a shorter average such as 2 to 10 periods. Usually the average true range atr is based on 14 periods and can be calculated on an intraday daily weekly or monthly basis.

How To Download Install Atr Indicator For Mt4 And Mt5

Scalping Forex Scalpingforex Forex Forex Trading System Binary

Choppiness Index Indicator Trading Strategy Stockmaniacs Trading Strategies Cryptocurrency Trading Trend Trading

Make 98 Profit Only In 30 Seconds Too Good To Be True With This Website You Can Trade And Make Easy Mercado De Acoes Investimento Investimento Financeiro

Monitoring Of Multiple Markets Timetotrade Community How To Get Rich Intraday Trading Online Trading

9qhdpc 41lowrm

Square The Range Trading System By Michael S Jenkins Sacred Traders Jenkins Trading System

Tiw8i54tv3y69m

S6k2u2mvvws6am

9tppj04maqj3km

S Viuxhhpoytgm

Doublecci Woodies Metatrader 4 Forex Indicator Forex Woodies Chart

My2 Nkyxrgutlm

5cpcp0pnkmxavm

Wbgqjz39xd6jxm

8i6qi7zjgmpfjm

Tjw0h Pg8afdm

An Introduction To True High True Low Average True Range Atr Is Known As A Volatility Indicator Which Was Blog Marketing Forex Trading Tips Stock Market

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gct6scdz3kdcinsn4yvc Samjfeq0bvpwp5ukrg38ppkt3unmy9q Usqp Cau

Npt1ruolpjw2lm

B Uy S3pqbrr6m

Vjhkl2ccgntr5m

Make 98 Profit Only In 30 Seconds Too Good To Be True With This Website You Can Trade And Make Easy An Trading Charts Stock Options Trading Forex Trading

Pin On 044 Investing Fintech

Pin On Forex

Forex Multi Moving Average Scalping Strategy Forexmt4systems Moving Average Forex Trading Strategies Forex Trading Tips

7quhtprxexofm

Weje59pm43alhm

P3kcg5gmyjhg7m

Zxa5l428kaf7nm

Day Trade To Win Youtube Day Trading Learning Chart

Wbgqjz39xd6jxm

About Tradingview Alerts Tradingview

7jmc4ago2fmbam

Positional Trading Scalp Trading Day Trading Intra Day Trading In 2020 Day Trading Trading Position Trading

Pin On Stock Market

Microeconomic Indicator In Forex Nfp Acronym Expansion Nonfarm Payrolls What Are Nonfarm Payrolls Bureau Of Labor Stati Payroll Forex Employment Statistics

What Is The Average Credit Card Interest Rate

S6k2u2mvvws6am

:max_bytes(150000):strip_icc()/close-up-of-man-hand-analyzing-stock-market-chart-1023021802-e5e288d56a9d412c8aa31cc6d908910b.jpg)

Determining Where To Set Your Stop Loss

Those Who Understand It Earn It Those Who Don T Pay It With Trend Trading A Trend Is A Function Of Time Com Trend Trading Trade Finance Business Finance

How To Download Install Atr Indicator For Mt4 And Mt5